What Are Three Ways to Obtain Funds for Long Term Capital Project?

Definition: Capital budgeting is the method of determining and estimating the potential of long-term investment options involving enormous upper-case letter expenditure. It is all almost the visitor's strategic conclusion making, which acts every bit a milestone in the business.

For Example; Let united states of america now consider upper-case letter budgeting for buying a new printing machine by a publishing house. The car is worth $15000 and will generate a return of $3000 annually. Thus the payback period of the machine is five years. The expected annual rising in aggrandizement is 10%.

Let us calculate the real investment value after the first year:

We can say that the company's actual profit after a year is estimated at $1636 instead of $3000.

Content: Capital Budgeting

- Features

- Factors

- Objectives

- Process

- Decisions

- Techniques

- Conclusion

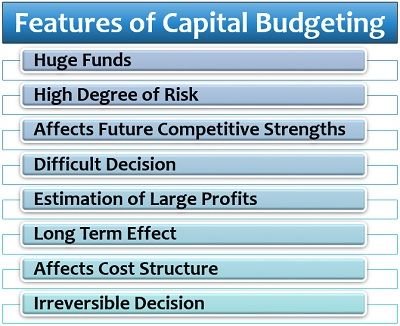

Features of Upper-case letter Budgeting

Upper-case letter budgeting is a crucial conclusion and to understand the concept in a better way, let united states of america get through its following features:

- Huge Funds: Uppercase budgeting involves expenditures of high value which makes it a crucial function for the management.

- High Caste of Adventure: To take decisions which involve huge financial burden tin be risky for the company.

- Affects Hereafter Competitive Strengths: The company's future is based on such capital expenditure decisions. Sensible investing can improve its competitiveness, whereas a wrong investment may lead to business organisation failure.

- Difficult Conclusion: When the future is dependant on capital letter budgeting decisions, it becomes difficult for the management to grab the most appropriate investment opportunity.

- Estimation of Big Profits: Any investment conclusion taken by the company is fabricated with the perspective of earning desirable profits in the long term.

- Long Term Effect: The effect of the decisions taken today, whether favourable or unfavourable, will be visible in the future or the long term.

- Affects Cost Structure: The visitor'south price structure changes with the capital budgeting; for instance, it may increase the fixed cost such equally insurance charges, involvement, depreciation, rent, etc.

- Irreversible Decision: A decision once taken is tough to be amended since it involves a loftier-value nugget which may not exist sold at the same price once purchased.

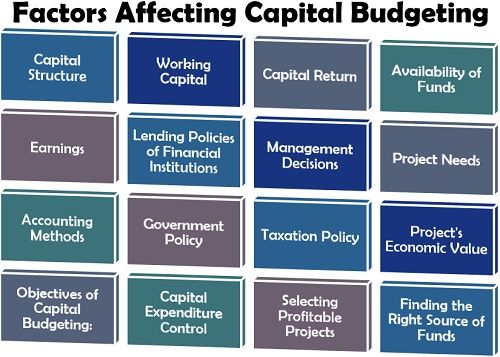

Factors Affecting Uppercase Budgeting

The capital budgeting decisions influenced by various elements present in the internal and external business environment. Post-obit are some of the meaning factors affecting investment decisions:

Capital Structure: The company'south capital structure, i.e., the composition of shareholder's funds and borrowed funds, determines its upper-case letter budgeting decisions.

Working Capital: The availability of capital required by the company to carry out day to mean solar day business operations influences its long-term decisions.

Capital letter Render: The management estimates the expected return from the prospective capital investment while planning the visitor's capital upkeep.

Availability of Funds: The company's potential for capital budgeting is dependant on its dividivent policy, availability of funds and the ability to acquire funds from the other sources.

Earnings: If the company has a stable earning, it may programme for massive investment projects on leveraged funds, just the aforementioned is not suitable in case of irregular earnings.

Lending Policies of Fiscal Institutions: The terms on which financial institutions provide loans such every bit interest rates, collateral, duration, etc. contributes to capital budgeting decisions.

Management Decisions: The decision of the direction to take a risk and invest funds in high-value assets or holding some other plan, also determines the capital letter budgeting of the company.

Project Needs: The company needs to consider all the essentials of a new projection. Also, the ways to fulfil the requirements forth with the estimate of the related expenses should be clear.

Bookkeeping Methods: The accounting rules, principles and methods of the company is another cistron considered while capital budgeting to frame the reporting of such expenses and revenue to be generated in futurity.

Authorities Policy: The restrictions imposed and the exemptions allowed by the authorities to the companies while investing in majuscule nature, impacts the company's upper-case letter budgeting decisions.

Taxation Policy: The taxation process and policy of the country also influences the long-term investment conclusion of the firm since additional capital volition exist required for such expenses.

Project'due south Economic Value: The total toll estimated for the long-term investment and the capacity of the company determines the majuscule budgeting decisions.

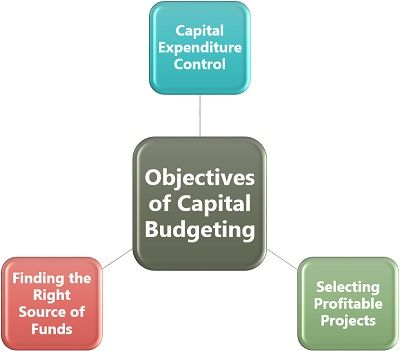

Objectives of Uppercase Budgeting

What is the demand for upper-case letter budgeting? Why do companies invest and then much fourth dimension and efforts in information technology? Capital budgeting is the long-term determination which affects the business organization to a peachy extent.

To know more than almost the necessity of capital letter budgeting for the companies, let us get through the post-obit objectives:

- Command of Capital Expenditure: Estimating the cost of investment provides a base to the management for controlling and managing the required capital expenditure accordingly.

- Selection of Profitable Projects: The company take to select the most suitable projection out of the multiple options available to it. For this, it has to keep in heed the various factors such as availability of funds, project's profitability, the rate of render, etc.

- Identifying the Correct Source of Funds: Locating and selecting the most appropriate source of fund required to make a long-term capital investment is the ultimate aim of uppercase budgeting. The management needs to consider and compare the cost borrowing with the expected return on investment for this purpose.

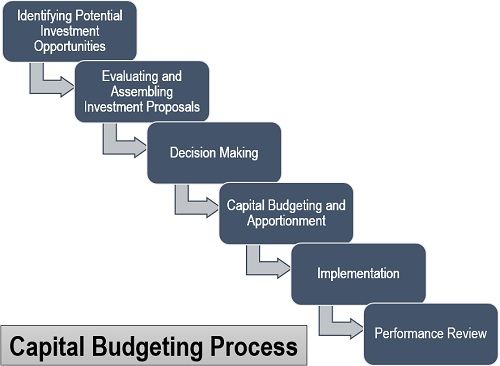

Capital Budgeting Process

Capital budgeting, as we know, is a conclusion making process. It involves the post-obit 6 steps:

Identifying Potential Investment Opportunities: The visitor has various options for capital employment on a long-term basis. In the initial stage, the direction needs to clarify the strengths and weaknesses of every project for foreseeing the potential of each selection.

Evaluating and Assembling Investment Proposals: In the next stride, the management assembles and compiles all the investment proposals on the grounds of price, adventure interest, time to come profits, render on investment, etc.

Decision Making: Now, the company needs to determine as to which investment choice it may select to suit its pocket and yield a high profit for the company in the long run.

Capital Budgeting and Apportionment: The next footstep is to classify the investment as per its duration. The long-term investment is mostly considered under uppercase budgeting. This stride helps in monitoring the functioning of an individual investment.

Implementation: After the apportioning of the long-term investment, the company comes into action for the execution of its determination. To avoid complications and excess time-consumption, the direction should lay out a detailed program of the project in advance.

Performance Review: The last but the about crucial step is the follow-upwardly and analysis of the project's performance. While the visitor'south operations are steady, the management needs to measure and correlate the bodily performance with that of the estimated one to figure out the difference and take cosmetic actions for the same.

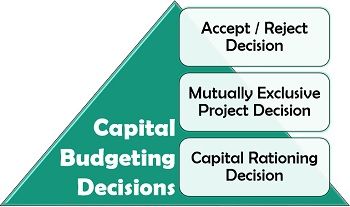

Majuscule Budgeting Decisions

The system's all capital budgeting decisions can be broadly categorized under the following 3 types:

- Take / Reject Determination: This blazon of arrangement is fundamental and mostly applies to the independent projects which are non affected by the acceptance possibility of other projects. The projects which generate a high charge per unit of return or toll of uppercase are accepted, and the plans which do not fulfil the criteria are rejected.

- Mutually Sectional Projection Decision: These projects compete with one another, i.eastward., the possibility of accepting one projection excludes the acceptance of the other.

- Capital Rationing Decision: The term itself explains that the limitation of capital dominates such decisions. In a situation where the firm has multiple investment options demanding huge funds, the management rank the projects on specific criteria; such as the rate of return of each project. Then, the projects with the highest per centum of profit or those which fulfil the requirements most tin can be selected.

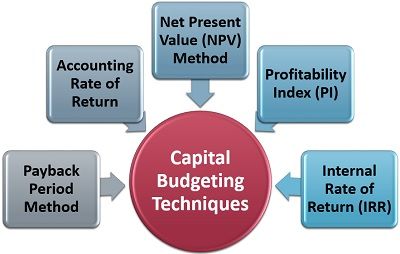

Majuscule Budgeting Techniques

Upper-case letter budgeting is a complicated and tedious process. It involves a lot of financial expertise and calculations. Following are the diverse computations required to determine the capital budgeting of a new project:

Payback Catamenia Method:

The payback period method is the simplest of all. It defines the period in which the company can recover its investment value.

The formula for calculating the payback menses of a project is:

![]()

The shorter is the payback period of the project, the more than suitable it is for the company.

Accounting Rate of Return:

The accounting rate of return depicts the future profitability of a project with the assist of accounting information mentioned in financial statements.

The formula for calculating the accounting rate of return is:

![]()

The higher is the ARR of the investment proposal, the more preferable it is for the company.

Net Nowadays Value (NPV) Method:

Net present value is the discounted cash flow method. It functions on the principle that the cash arrival from the projection will be acquired in a future menstruation when the value of money will change. Hence, the future cash catamenia needs to be discounted now value to compare the estimate functioning with the bodily 1.

The Net Present Value (NPV) formula is:

![]()

i.e.,

![]()

Where, A1, A2, A3 are the cash inflows in sequent years;

k is the toll of capital letter of the projection;

We assume that all the cash outflows are washed in the first year (t) and therefore, t=1.

Profitability Index (PI):

Profitability index is the ratio which relates the present value of earnings with the investment value.

The formula of the Profitability Index (PI) is:

![]()

or,

![]()

To denote the Profitability Index in percentage, Profitability Ratio of a new project is calculated. Its formula is:

![]()

Internal Charge per unit of Return (IRR):

The internal rate of return determines the charge per unit at which the investment amount is recovered by the cash inflows. The net present value of the project is zero in this method. Too, the discounted cash inflow and outflow are the same.

Initially, the Present Value of Cash Outflow (Co) is calculated as follows:

![]()

Where Co is the present value of greenbacks outflow;

C1, C2, C3 are the cash inflows in the sequent years;

due north is the number of years;

r is the expected rate of render.

This is the cutoff charge per unit of the project.

The Internal Rate of Return (IRR) formula is:

![]()

Where NPV (LR) is the net present value at a lower charge per unit;

NPV (60 minutes) is the net present value at a higher rate.

Analysis: If the IRR≥Co, the projection is accustomed; simply if IRR<Co, the projection is rejected.

Conclusion

Uppercase budgeting is a vital part of all the organizations, whether big or small. These decisions build the foundation of any concern. With a single fault in capital budgeting, the visitor may stop upward into huge loss and vice-versa.

Source: https://theinvestorsbook.com/capital-budgeting.html

0 Response to "What Are Three Ways to Obtain Funds for Long Term Capital Project?"

Post a Comment